We’ve figured out how to unredact some of the Epstein Files:

Trump's DOJ is so incompetent that they don't even know how to properly redact PDFs.

Below you will see some of the pages we Unredacted:

Unredacted Version:

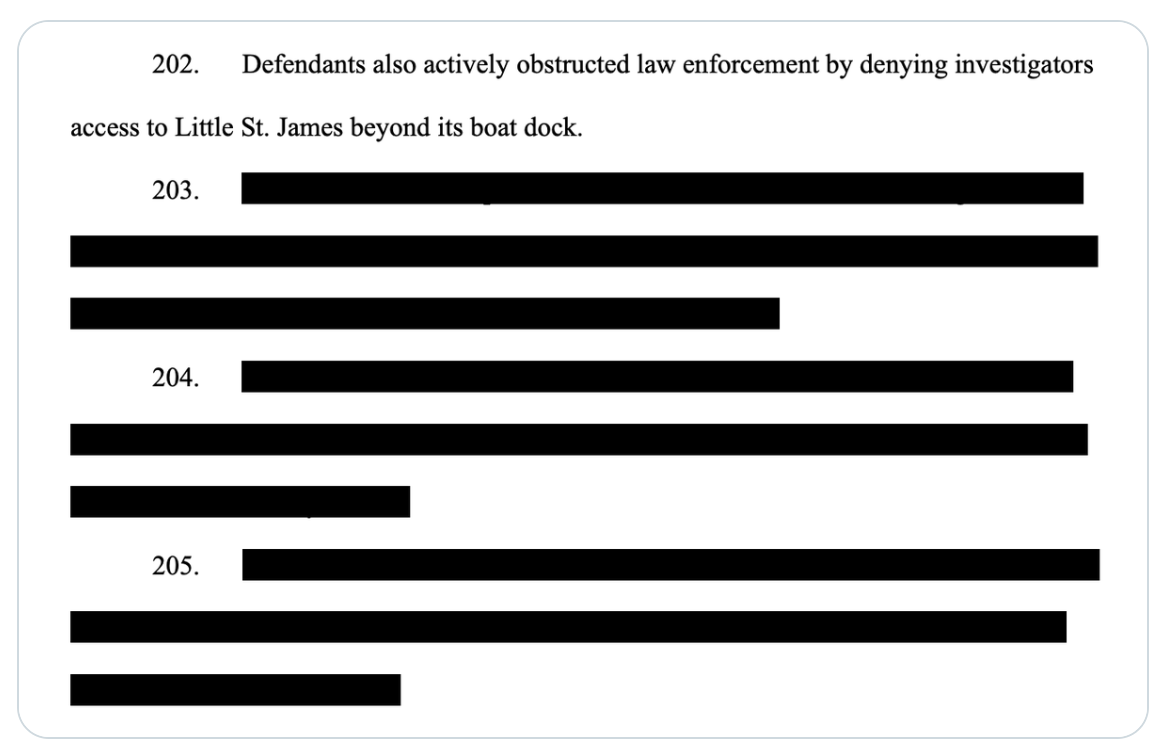

202. Defendants also actively obstructed law enforcement by denying investigators access to Little St. James beyond its boat dock.

203. Defendants also attempted to conceal their criminal sex trafficking and abuse conduct by paying large sums of money to participant-witnesses, including by paying for their attorneys’ fees and case costs in litigation related to this conduct.

204. Epstein also threatened harm to victims and helped release damaging stories about them to damage their credibility when they tried to go public with their stories of being trafficked and sexually abused.

205. Epstein also instructed one or more Epstein Enterprise participant-witnesses to destroy evidence relevant to ongoing court proceedings involving Defendants’ criminal sex trafficking and abuse conduct.

Unredacted Version:

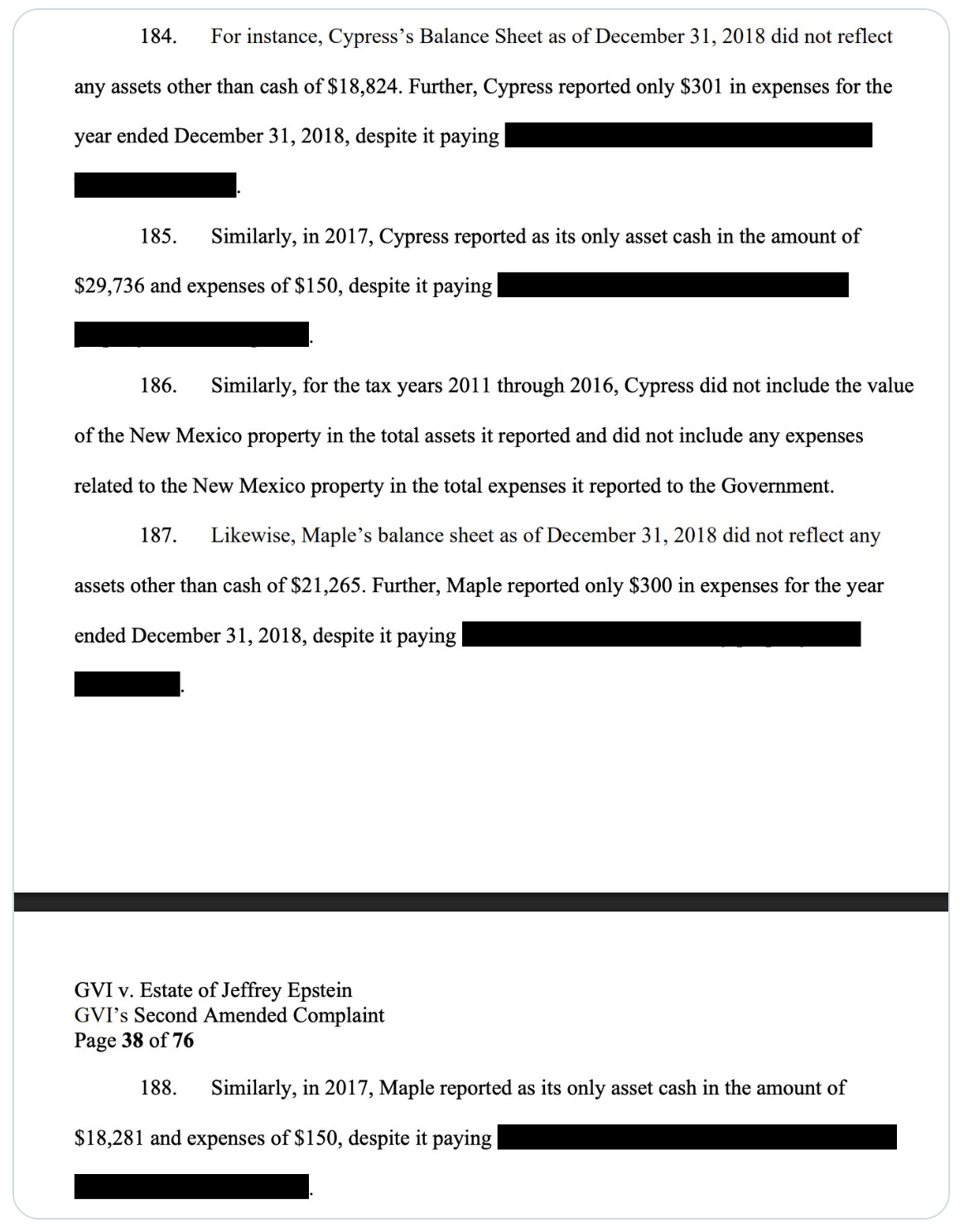

184. For instance, Cypress’s Balance Sheet as of December 31, 2018 did not reflect any assets other than cash of $18,824. Further, Cypress reported only $301 in expenses for the year ended December 31, 2018, despite it paying $106,394.60 in Santa Fe property taxes on November 6, 2018.

185. Similarly, in 2017, Cypress reported as its only asset cash in the amount of $29,736 and expenses of $150, despite it paying $55,770.41 and $113,679.56 in Santa Fe property taxes during 2017.

186. Similarly, for the tax years 2011 through 2016, Cypress did not include the value of the New Mexico property in the total assets it reported and did not include any expenses related to the New Mexico property in the total expenses it reported to the Government.

187. Likewise, Maple’s balance sheet as of December 31, 2018 did not reflect any assets other than cash of $21,265. Further, Maple reported only $300 in expenses for the year ended December 31, 2018, despite it paying $336,471.87 in New York City property taxes during 2018.

188. Similarly, in 2017, Maple reported as its only asset cash in the amount of $18,281 and expenses of $150, despite it paying $327,497.48 and $6,487.04 in New York City property taxes during 2017.

Unredacted version:

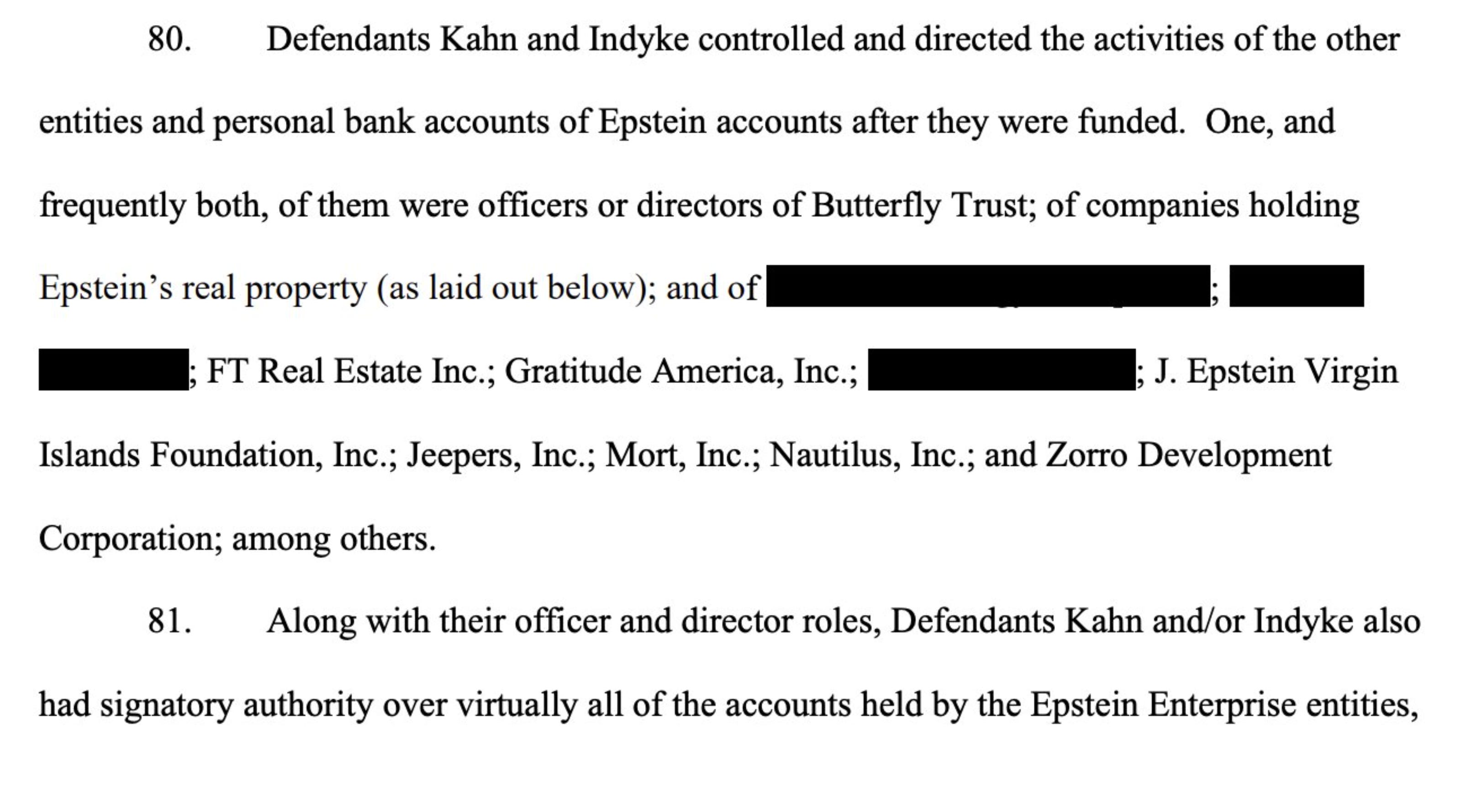

"80. Defendants Kahn and Indyke controlled and directed the activities of the other entities and personal bank accounts of Epstein accounts after they were funded. One, and frequently both, of them were officers or directors of Butterfly Trust; of companies holding Epstein’s real property (as laid out below); and of [[Financial Strategy Group, Ltd.; Financial Trust, Inc.;]] FT Real Estate Inc.; Gratitude America, Inc.; [[Hyperion Air, Inc.; ]] J. Epstein Virgin Islands Foundation, Inc.; Jeepers, Inc.; Mort, Inc.; Nautilus, Inc.; and Zorro Development Corporation; among others."

Unredacted Version:

UNREDACTION OF BELOW DOCUMENT:

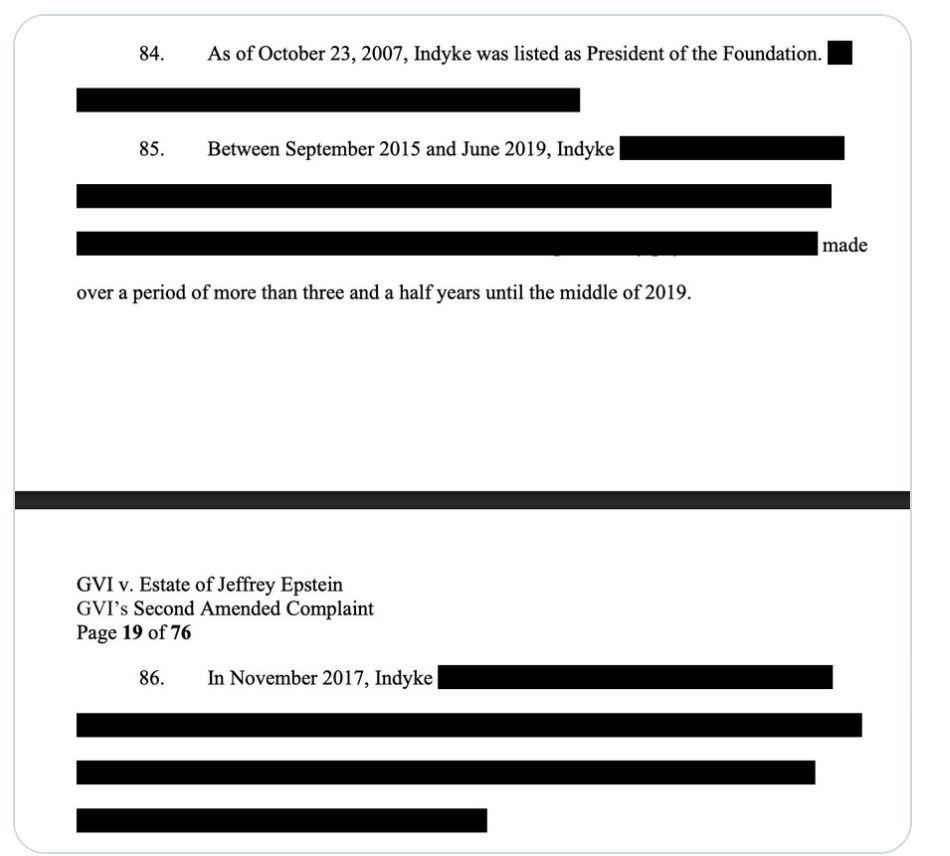

84. As of October 23, 2007, Indyke was listed as President of the Foundation. He also was a signatory on the Foundation’s checking accounts.

85. Between September 2015 and June 2019, Indyke signed Foundation account checks for over $400,000 made payable to young female models and actresses, including a former Russian model who received over $380,000 through monthly payments of $8,333 made over a period of more than three and a half years until the middle of 2019.

■ GVI v. Estate of Jeffrey Epstein GVI’s Second Amended Complaint Page 19 of 76

86. In November 2017, Indyke signed a Foundation check made payable to the immigration lawyer in New York who was involved in one or more forced marriages arranged among Epstein’s victims to secure a victim’s immigration status. The check’s memo line references the former Russian model’s last name.

Unredacted Version:

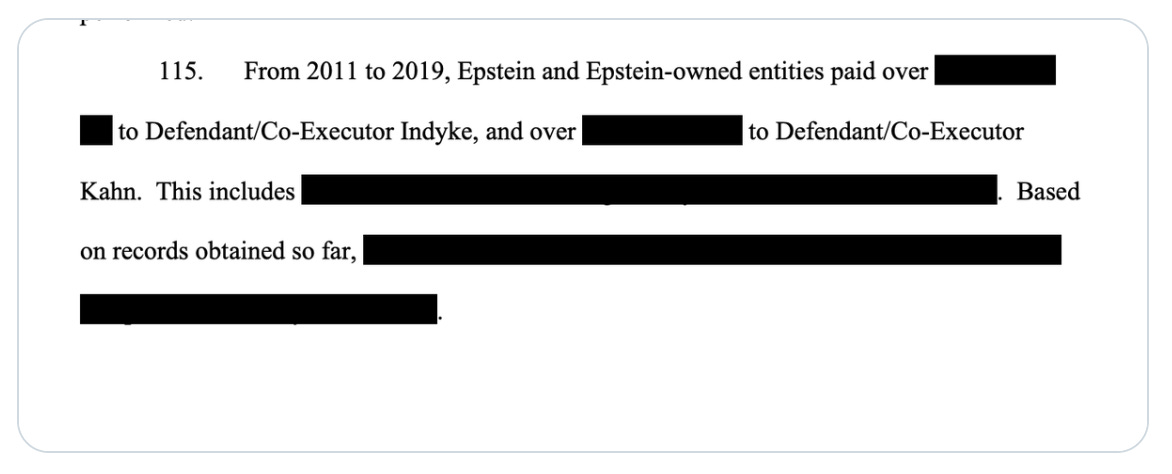

115. From 2011 to 2019, Epstein and Epstein-owned entities paid over $16 million net to Defendant/Co-Executor Indyke, and over $10 million net to Defendant/Co-Executor Kahn. This includes loans that are still outstanding to Indyke- and Kahn-related entities. Based on records obtained so far, tax forms provided by Epstein entities did not report nearly the full compensation to Indyke and Kahn.

Unredacted Version:

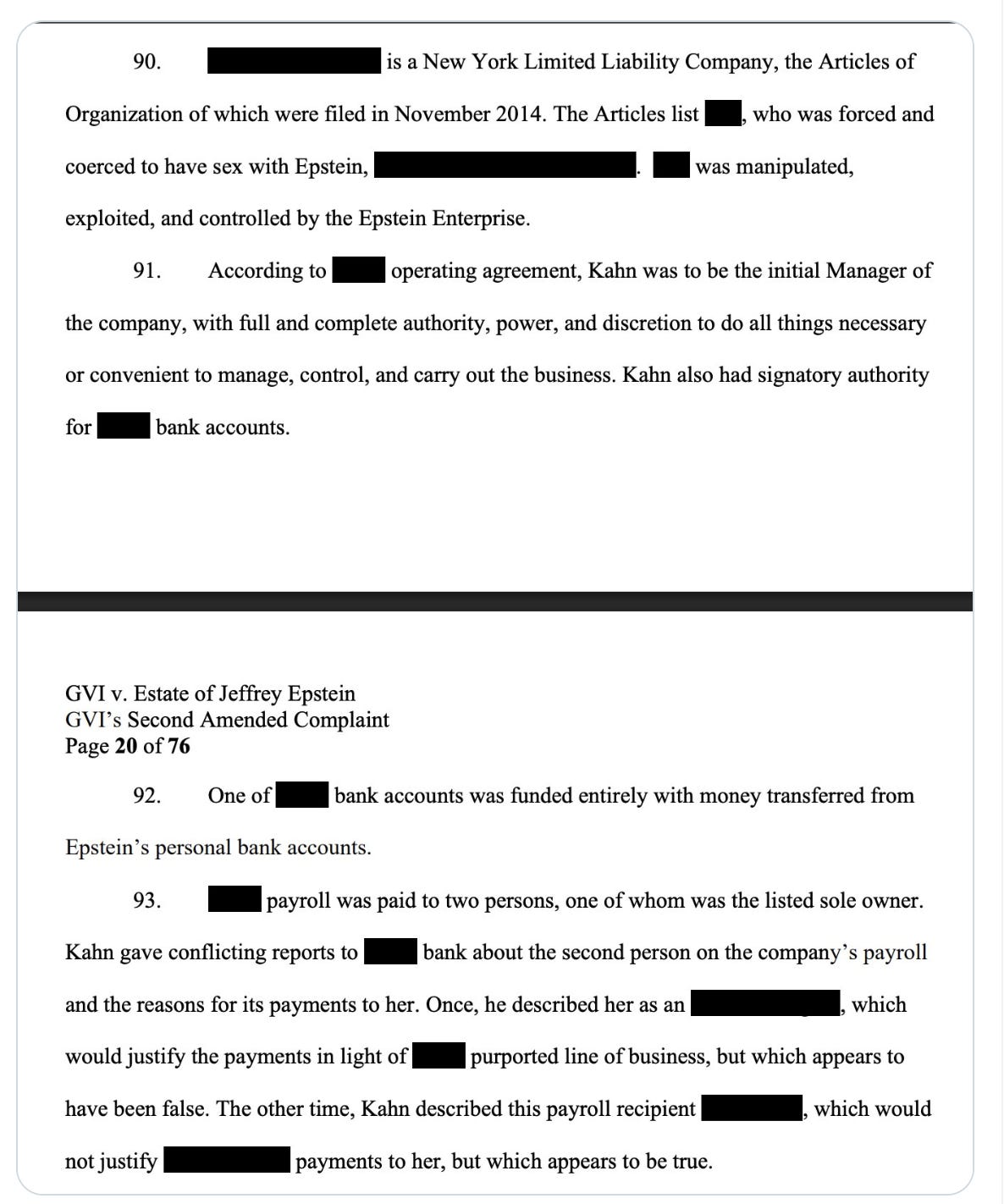

90. JSC Interiors, LLC is a New York Limited Liability Company, the Articles of Organization of which were filed in November 2014. The Articles list JSC, who was forced and coerced to have sex with Epstein, as the company’s sole owner. JSC was manipulated, exploited, and controlled by the Epstein Enterprise.

91. According to JSC’s operating agreement, Kahn was to be the initial Manager of the company, with full and complete authority, power, and discretion to do all things necessary or convenient to manage, control, and carry out the business. Kahn also had signatory authority for JSC’s bank accounts. 1111 1111 • • GVI v. Estate of Jeffrey Epstein GVI’s Second Amended Complaint Page 20 of 76

92. One of JSC’s bank accounts was funded entirely with money transferred from Epstein’s personal bank accounts.

93. JSC’s payroll was paid to two persons, one of whom was the listed sole owner. Kahn gave conflicting reports to JSC’s bank about the second person on the company’s payroll and the reasons for its payments to her. Once, he described her as an interior designer, which would justify the payments in light of JSC’s purported line of business, but which appears to have been false. The other time, Kahn described this payroll recipient as a dentist, which would not justify JSC Interiors’ payments to her, but which appears to be true.

Tiktok failed to load.

Tiktok failed to load.Enable 3rd party cookies or use another browser